US Collectible Toy Market & Southeast Asia Manufacturing Shift: 2026 Sourcing Guide

The US Collectible Toy Market Has Moved to Southeast Asia: What Sourcing Teams Need to Know in 2026

The American collectible toy market grew into an estimated $5.5 to $7.3 billion industry by 2024, and adult collectors deserve most of the credit. This demographic now accounts for nearly 30% of total toy sales, representing an estimated $9 billion in annual spending from consumers who technically outgrew the toy aisle decades ago.

For brands and retailers watching their margins, the "China+1" supply chain strategy is no longer a future-proofing exercise - it's the new baseline - and the results are now clear. Hasbro sourced 90% of its products from China in 2012; that figure dropped to approximately 50% by mid-2025, with plans to reduce further to around 30% by 2026. Funko moved aggressively as well, significantly reducing its China production through an intensive transition to Vietnam, Cambodia, and Indonesia alternatives.

The math behind this manufacturing shift changed dramatically over the past two years. Southeast Asian countries like Vietnam and Indonesia continue to offer 30% to 50% lower labor costs than China, but the tariff differential became the deciding factor. As of mid-2025, Chinese toys face tariffs exceeding 30%, while Vietnamese and Indonesian goods come in at 19% to 20%. That gap directly impacts landed costs and competitive positioning for every product line. Note that tariff rates remain subject to ongoing trade negotiations and may fluctuate even further.

Understanding the Three Major Collectible Toy Segments

Action Figures and Vinyl Collectibles

Action figures and vinyl collectibles dominate the collectible toy space, generating an estimated $3 billion domestically and representing approximately 45% of the entire segment. Funko generated $1.05 billion in 2024, controlling an estimated 65% of the collectible figurines market with a catalog now exceeding 14,000 unique Pop! designs. At the premium end, Hot Toys commands $300 to $800+ for a single figure, while standard Funko Pops retail for $11 to $15. This segment continues expanding at an estimated 6% to 9% annually, with adults 15 and older making nearly 44% of purchases.

For brands developing action figures and vinyl collectibles, Vietnam has proven itself as the preferred manufacturing destination. The country's factories demonstrated their capability through partnerships with industry leaders throughout 2024 and 2025, and experienced toy sourcing partners like Play Trail can connect brands with vetted facilities that specialize in the paint applications, articulation, and packaging quality this segment demands. At Play Trail, we've already helped major US brands shift production away from China. One of our customer’s first batch of collectible toys made in Vietnam will hit shelves in Q2 of this year!

Trading Cards

Trading cards have become a phenomenon unto themselves. The global trading card game market reached an estimated $7.5 billion in 2025, with Pokémon sitting at the top as the highest-grossing media franchise in history at an estimated $150 billion or more in lifetime revenue as of late 2024. PSA processed over 15 million card submissions for grading in 2024, with the overall industry seeing approximately 16% growth compared to 2023 across major grading companies. Prices span everything from $4 to $8 booster packs to six-figure auction results, with vintage cards like the 1999 Charizard First Edition commanding $300,000+. North America represents over 40% of global trading card sales.

Building Sets and LEGO Collectibles

Building sets and LEGO collectibles posted the fastest growth of any category at 16% in 2024, marking five consecutive years of expansion that continued into 2025. LEGO's global revenue exceeded $10 billion in 2024, up 13% year over year, with adult-focused sets generating a third of the company's sales by value. The LEGO Icons 18+ line has grown to over 150 sets, with collectors paying $350 to $850 for premium releases like the Millennium Falcon and Titanic.

LEGO's $1.3 billion investment in its Binh Duong, Vietnam facility - which officially opened in April 2025 and is set to employ approximately 4,000 workers - validated that Southeast Asian manufacturing can handle the precision tolerances this category requires, opening doors for other building set brands that have since followed with regional diversification.

The "Kidult" Factor Driving Growth

The "kidult" phenomenon ties all three segments together. In Q1 2025, adults spent an estimated $1.8 billion on toys for themselves, more than any other age group, and this trend has continued into 2026. When surveyed, 63% cite nostalgia as their main motivation. These buyers represent only 25% of purchasers but drive an estimated 60% of the industry's dollar growth, making premium quality and collector-grade finishing non-negotiable for brands targeting this demographic.

Why China's Manufacturing Dominance Has Eroded

Chinese factories still control roughly 70% to 75% of global toy production, down from nearly 80% in 2020, and supply approximately 70% of US toy imports - a figure that continues declining as diversification accelerates. Guangdong province hosts over 5,500 toy factories employing more than a million workers, though consolidation has increased as smaller facilities struggle with rising costs.

Scale alone doesn't explain China's staying power. The real advantage has been vertical integration, with raw materials, mold-making, electronics components, painting facilities, and packaging operations all existing within a single region. Standard production takes 4 to 8 weeks compared to 6 to 12 weeks in Vietnam, minimum order quantities stay flexible at 500 to 1,000 units, and component suppliers can deliver in one day.

But structural pressures intensified dramatically through 2024 and 2025. Manufacturing wages in China climbed past $6.50 per hour, translating to $700 to $800 monthly. As of mid-2025, tariffs on Chinese toys exceed 30% when you stack the base MFN rate of 0% to 6.4% on top of Section 301 duties and the fentanyl tariff. During peak tensions in early 2025, combined rates briefly spiked significantly higher before negotiations stabilized the situation.

The shift accelerated meaningfully in 2024 and 2025, with China's share of US and EU toy imports dropping from 82% in 2019 to approximately 75% by late 2025. Chinese factory delegations visiting Vietnam nearly tripled in 2024 as manufacturers scouted alternative capacity, and many of those scouting trips have since converted to active production relationships.

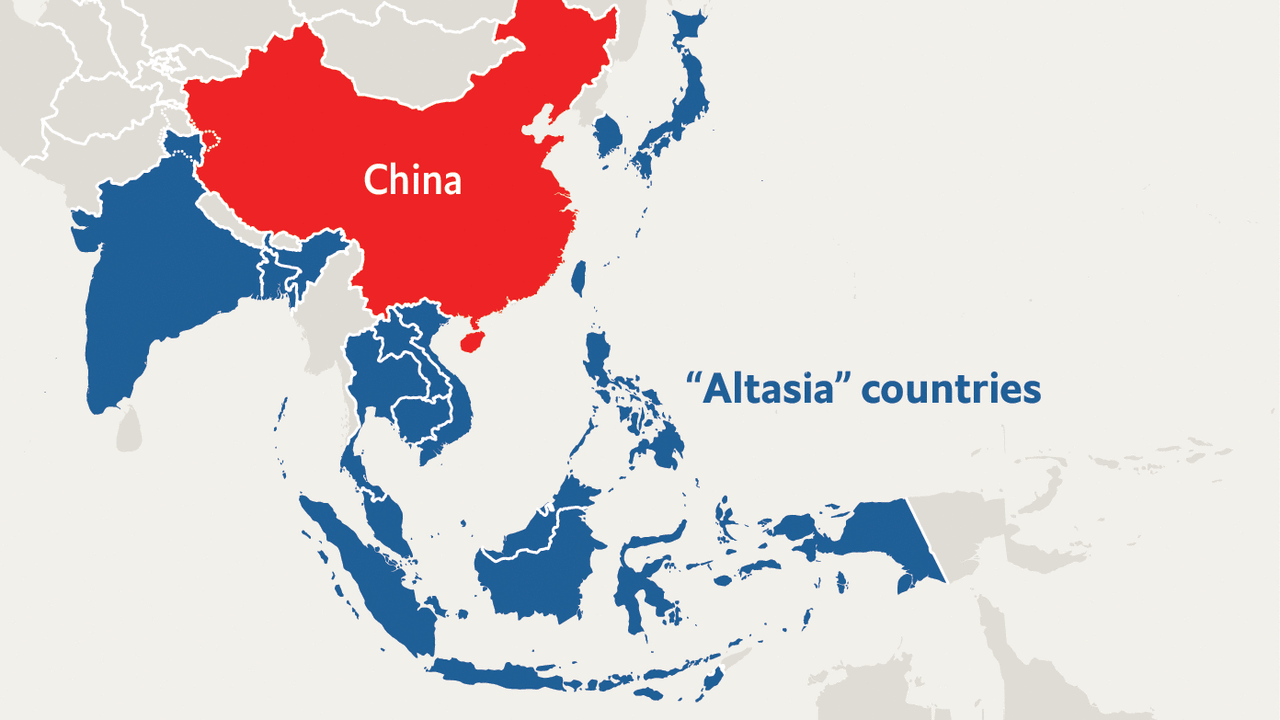

Vietnam: The Upcoming Leader for Toy Manufacturing

Vietnam now ranks second globally in toy exports, surpassing an estimated $4 billion in 2025. The country has over 180 export-capable factories, up from approximately 160 at the start of 2025, and the manufacturing base continues growing. Labor costs average $1.85 to $2.00 per hour, working out to $300 to $350 monthly - a significant discount versus China that has remained stable.

For collectibles specifically, Vietnam proved itself through manufacturers like GFT Group, which reportedly operates 5 factories in Hai Phong and Hai Duong with an estimated 15,000 workers producing approximately 9 million units monthly. Their reported client roster includes Funko, Hasbro, Mattel, Spin Master, and Schleich. LEGO's massive $1.3 billion Binh Duong investment, now employing workers with plans to reach approximately 4,000, demonstrated that Vietnam handles high-precision manufacturing at scale.

Infrastructure has fully caught up to support this growth. Hai Phong Port handles over 7 million TEUs annually, ranking among the top 30 globally. Cai Mep's deep-water port offers direct US routes without transshipping through Singapore, with shipping to the US West Coast taking 14 to 18 days - competitive with China.

For brands exploring Vietnam toy manufacturing, the challenge isn't finding factories but finding the right ones. Production capabilities, quality systems, and experience with Western compliance requirements vary significantly across facilities. This is where working with an established Vietnam-based toy sourcing company becomes valuable. Play Trail maintains direct relationships with vetted manufacturers across Vietnam's major production regions, helping brands navigate factory selection, quality benchmarking, and production oversight without the costly trial-and-error that comes with going it alone.

Trade policy remains something to monitor. The initial 46% reciprocal tariff threatened the entire Vietnam advantage until bilateral negotiations brought it down to 20% in July 2025, where it has since stabilized as of this writing. Vietnam's trade surplus with the US exceeded $115 billion in 2025, which guarantees continued scrutiny from Washington in 2026 and beyond.

Other countries in Southeast Asia: Strategic Alternatives for Specific Categories

Indonesia for Dolls and Volume Production

Indonesia holds the third spot globally with an estimated 3% to 4% market share and manufactures approximately half the world's toy dolls. Mattel's Cikarang facility, one of the largest toy factories on Earth, has capacity to produce up to 3 million Barbie dolls weekly with a workforce reaching 9,000+ during peak season. This single plant accounts for over 35% of Indonesia's total toy exports.

Labor costs in Indonesia remain among the lowest in the region. Central Java minimum wages run $140 to $190 monthly, while manufacturing centers like West Java average $260 to $330 - representing 30% to 40% savings versus coastal China. The negotiated US tariff rate of 19% (reduced from 32% in 2025) makes Indonesia increasingly attractive for volume production. The country has also developed strong injection molding and die-cast capabilities.

Play Trail's network extends into Indonesia's key manufacturing zones, giving brands access to the production capacity and cost structures that have made the country a destination for major toy companies. For brands considering dolls, die-cast vehicles, or high-volume items, Indonesia often delivers the optimal balance of cost, capability, and tariff treatment.

Thailand and Malaysia: Supporting Roles

Malaysia benefits from CPTPP membership for non-US markets, though higher wages (minimum $410+ monthly) push manufacturers toward premium plush and educational toys. Thailand has excellent infrastructure through its Eastern Economic Corridor but lacks significant collectible toy capacity, though Play Trail monitors developments across Thailand's manufacturing sector for brands exploring regional options.

How Major Toy Brands Restructured Their Supply Chains

The industry's biggest companies poured billions into geographic diversification, and their experiences over the past several years offer a roadmap for firms still in transition.

Hasbro started early, spreading production across 8+ countries including 10+ factories in Vietnam, 11 in India, and domestic US facilities. They cut China sourcing from 90% in 2012 to approximately 50% by mid-2025, with targets to reach approximately 30% by 2026. The company has delivered $400+ million of a planned $1 billion cost-savings program and achieved significant tariff cost mitigation.

Mattel invested over $50 million in a Mexican "mega-factory" spanning 200,000 square meters with 3,500 workers, now their largest global facility. The company achieved its target structure where no single country exceeds 25% of global manufacturing and reduced its China factory count from four to one by the end of 2025.

Funko demonstrated how quickly companies can move when motivated. The company significantly reduced its China sourcing through 2024 and 2025, pivoting to Vietnam, Cambodia, and Indonesia alternatives. Their model of exclusively third-party manufacturing with no long-term contracts gave them flexibility to execute this transition. They absorbed approximately $40 to $45 million in tariff costs during 2025 despite the aggressive transition.

Spin Master achieved its target of sourcing 70% of US toys from outside China by late 2025 and is now pushing toward 80% through 2026, up from 45% in early 2025. MGA Entertainment, the company behind L.O.L. Surprise!, executed its plan announced in April 2025 to shift 40% of manufacturing to India, Vietnam, and Indonesia.

The common thread across all these transitions is that successful diversification required local expertise. Brands that attempted to replicate their China sourcing relationships independently in Southeast Asia frequently encountered quality inconsistencies, communication challenges, and compliance gaps that eroded expected cost savings.

Building Your Southeast Asia Toy Sourcing Strategy in 2026

The market outlook remains strong, with global collectibles projected to grow at an estimated 10% to 11% annually to reach $45 to $50 billion by 2032. The US toy market should expand to approximately $43 billion by 2033, with collectibles outperforming the broader category.

Supply chain transformation continues accelerating through 2027 as manufacturers push toward 75% to 85% non-China production. Vietnam's factory count is growing from 180+ toward an estimated 220+ export-level facilities by year-end. India is emerging as a significant alternative despite learning curves, and Mexico nearshoring continues intensifying for North American distribution.

Key Risks to Monitor in 2026

Several factors bear watching as you develop your sourcing strategy. Vietnam's substantial trade surplus invites potential tariff escalation - this remains the most significant policy risk. Quality consistency challenges persist during manufacturing transitions, though the learning curve has flattened as best practices spread. Component supply chains often still trace back to Chinese inputs, as Vietnamese factories frequently source parts from across the border. And the tariff landscape could shift again with changing trade policies or a new administration's priorities.

Recommended Approach for Diversification

Companies still evaluating Southeast Asian partnerships should consider an accelerated transition over 18 to 24 months in 25% to 30% increments - the phased approach has been validated, though firms starting in 2026 may need to move faster than early movers did. Keeping some China capacity for component access and quality benchmarking remains advisable. Here's how the regional options align with different product categories:

Vietnam remains the primary destination for established collectible categories including action figures, vinyl collectibles, and building sets. The manufacturing ecosystem has matured significantly, and proven OEM partners exist across major product types. Play Trail's Vietnam-based team provides on-the-ground support for factory qualification, production monitoring, and quality assurance, reducing the transition risks that come with establishing new manufacturing relationships.

Indonesia works well for dolls, die-cast products, and volume production, leveraging the infrastructure and workforce that Mattel and other major brands developed over decades.

The Philippines suits detail-intensive collectibles requiring close design collaboration and premium finishing, where English-language communication and skilled labor offset somewhat higher costs.

Mexico handles bulky items like ride-ons and outdoor toys where USMCA proximity and duty-free treatment offset higher labor costs.

Budget Appropriately for the Transition

Budget for 15% to 20% higher quality control costs during the transition period, including resident quality engineers for the first 12 to 18 months. This premium has decreased slightly from 2024 levels as the regional manufacturing base has matured. Working with an experienced sourcing partner can reduce these costs further by leveraging existing quality infrastructure and factory relationships rather than building oversight capability from scratch.

Most importantly, don't let any single country exceed 25% of production. Geographic concentration creates its own risks, as the tariff volatility of 2024 and 2025 demonstrated.

Target Portfolio Structure for 2027

A reasonable 2027 production portfolio - achievable within the next 12 to 18 months for committed firms - might look like: 15% to 20% in China for component access and quality benchmarking, 30% to 40% in Vietnam for core collectibles, 15% to 20% in Indonesia for volume production, 15% to 20% in Mexico for nearshore capacity, and 10% to 15% in India or the Philippines for diversification.

Companies that started this process in 2018 to 2020 hold structural advantages and have locked in preferred factory relationships. However, Funko's 2024-2025 experience showed that aggressive action can deliver meaningful results within 12 to 18 months for firms willing to commit. The question for companies still primarily China-dependent in 2026 is not whether to diversify, but how quickly they can execute.

The Bottom Line for Toy Sourcing Teams

The collectible toy market's fundamentals remain solid. Adult collectors drive an estimated 60% of industry dollar growth, licensed merchandise represents over a third of sales, and premiumization continues across action figures, trading cards, and building sets.

The supply chain transformation, however, is now well underway. Chinese tariffs exceeding 30% (as of mid-2025) have eliminated the cost advantage that once made diversification optional. Vietnam and Indonesia offer 10 to 15 percentage points of tariff savings along with 30% to 50% labor cost reductions, and established manufacturing relationships reduce transition risk.

Multi-country sourcing has become standard practice among industry leaders, with most now operating structures where no single source exceeds 25% of production. Companies that haven't begun transitioning face margin compression and competitive disadvantage against peers who secured alternative capacity in 2024 and 2025.

The window for establishing Southeast Asian partnerships at favorable terms remains open in 2026, but capacity constraints are tightening as demand for non-China manufacturing accelerates across consumer goods categories. First-mover advantages in factory relationships have largely been claimed - but quality partners still have capacity for brands willing to move decisively.

Ready to explore your Southeast Asia sourcing options? Play Trail's team has spent years building relationships with qualified toy manufacturers across Vietnam, Indonesia, and Thailand. Whether you're beginning to diversify from China or optimizing an existing multi-country strategy, we can help you identify the right factory partners, manage quality during transitions, and navigate the complexities of regional production. [Contact Play Trail Now] to discuss your sourcing requirements.

At PLAY TRAIL, we specialize in delivering end-to-end design, supply chain and manufacturing solutions that are tailored to meet your unique business objectives in toys and toys packaging production in Vietnam and Southeast Asia.

Let us help you simplify your supply chain, improve operational efficiency, and build a sustainable future. Our hands-on team is here to provide expert guidance and actionable insights that drive tangible results for your business.

Get in Touch Today

Whether you need assistance with sourcing, logistics, or end-to-end supply chain management, we’re here to help.

Contact us today for a free quote to make the right, optimal decisions for your business growth.